Sierra Wireless (NASDAQ:SWIR), the provider of wireless and intelligent connectivity solutions, has been beaten down badly over the past month and a half after releasing its second-quarter results early in August. This was despite the fact that Sierra beat consensus estimates on both the top and bottom lines last quarter.

It looks like investors are getting discouraged by the fact that Sierra is no longer delivering top line growth. In fact, last quarter, Sierra’s top line dropped 1% on a year-over-year basis as it is witnessing weakness in certain areas.

The OEM business is not generating growth

Sierra Wireless has witnessed gross margin erosion in recent months, while its revenue has also plunged owing to soft sales in its biggest business segment – OEM solutions. This particular segment accounts for almost 85% of Sierra’s top line, so a year-over-year drop of 4% in revenue in this segment is negatively impacting the company’s results.

What’s more, despite operating in a fast-growing space such as the Internet of Things, Sierra has been witnessing a slowdown in its revenue growth of late. Additionally, its gross margin is going down, which is not fit for a company that trades at 109 times last year’s earnings:

|

Period Ending |

31-Dec-15 |

31-Dec-14 |

31-Dec-13 |

|

Total Revenue (in millions) |

$607.80 |

$548.50 |

$441.80 |

|

Annual increase in revenue from prior year |

11% |

24% |

|

|

Cost of Revenue (in millions) |

$413.90 |

$369.50 |

$296.20 |

|

Gross Profit (in millions) |

$193.80 |

$178.90 |

$145.60 |

|

Gross Profit % |

31.90% |

32.60% |

33.00% |

Source: Sierra Wireless

In the latest quarter, Sierra’s OEM solutions business suffered due to demand weakness from one of its key customers in the automotive segment. This is a trend that has continued for three quarters now.

Of course, credit needs to be given to Sierra Wireless for consistently coming out with new products in this segment, such as the partnership with the Movimento Group to provide over-the-air software updates to electronic control units (ECUs) found in cars and trucks. But, it is likely that Sierra’s growth in the long run will be driven by its other two segments — Enterprise Solutions and Cloud & Connectivity Services — which currently account for just 15% of overall revenue at present.

When small is big

Sierra Wireless might be generating the majority of its revenue from the OEM solutions business, but this is not where the money is in the long run. In comparison, Sierra’s Enterprise and Cloud segments are the ones that are growing at a much faster pace and also carry greater margins. Last quarter, the Enterprise Solutions business grew 10% year-over-year, while Cloud and Connectivity witnessed a 47% increase.

More importantly, both these segments illustrated robust margins. The gross margin in the Enterprise Solutions business was 53.9% last quarter, up from 52.6% in the prior-year period, while Cloud and Connectivity delivered 40.7% gross margin. These margin figures are way higher than the OEM solutions segment, where the gross margin was 31% last quarter.

The reason behind higher margins in these two segments is Sierra’s focus on driving service sales, which carry low costs to implement. Looking ahead, Sierra should see acceleration in sales in both these segments on the back of its recent product launches that will help it capitalize on unique market opportunities in the service segment.

Smart SIM can disrupt the market

Back in February this year, Sierra Wireless unveiled the Smart SIM and connectivity service. This SIM card is based on the Quality of Service (QoS) networking platform, which automatically selects the best available service provider rather than steering the user toward a fixed service provider. Since Sierra Wireless has penned agreements with multiple operators, it means that its customers won’t have to suffer from outages since the Smart SIM is capable of switching to a superior network quickly.

Using this product, Sierra Wireless can tap a vast market for SIM cards that’s gaining traction due to the proliferation of wearable devices. By 2020, it is forecasted that annual SIM card shipments will hit 5.6 billion units driven by an increase in sales of health bands, smartwatches, and other wearables, when McKinsey forecasts that SIM card sales will generate $9.2 billion in revenue.

The acceptance of SIM cards in wearable devices will rise as Internet of Things gains momentum. Internet of Things devices always need to be connected to the internet to transmit data based on sensor inputs, which is why the need for SIM cards in such devices will increase going forward. More specifically, Sierra Wireless will be able to tap the market for embedded SIM cards going forward, which are either soldered into devices or plugged-in the traditional way.

This is because the connectivity service provided by Sierra’s Internet of Things application platform is open in nature, and therefore allows the customers to manage third-party SIM cards on the same platform.

Therefore, by bringing a Smart SIM to the market, Sierra Wireless will also be able to tap customers who use dual SIM phones. This, again, is a fast-growing market that’ll grow at a pace of 17% a year until 2020. Since Sierra is offering a solution that combines multiple networks in just one SIM card, users won’t have the hassle of keeping more than two SIM cards in their phones.

Why Smart SIM is a big deal

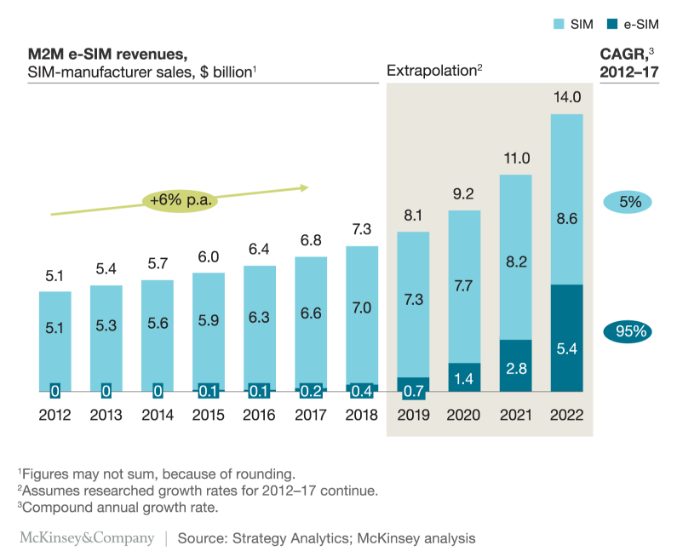

Sierra Wireless’ Smart SIM offering could turn out to be a big deal in the future. This is because the product will allow it to not only benefit from the growing sales of SIM cards, but also from embedded SIM cards that are expected to gain traction in the future on the back of wearable devices. The following chart shows the expected growth of the SIM card market over the coming years, illustrating Sierra Wireless’ business opportunity:

{kind=link}

Thus, by 2022, it is estimated that the overall SIM card market will be worth $14 billion. Of this, $5.4 billion revenue will be generated by e-SIMs as their adoption will grow at a tremendous pace. On the other hand, traditional SIM cards will continue to account for the major share of the market. Therefore, with its Smart SIM solution, Sierra Wireless can foray into a really big market that could drive its revenue and margins in the long run.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.