As implied by the corporate’s FY 2016 Annual Report title, “Leading a Digital Industrial Era,” General Electric (NYSE:GE) is shifting full velocity forward growing a portfolio of data expertise services and products by way of its GE Digital enterprise phase, which operates horizontally throughout the corporate. Particularly, GE is in search of to develop and develop its Predix expertise model which (broadly) helps the seize, storage, evaluation, and exploitation of machine-generated knowledge.

This marriage of producing experience and digital applied sciences is a logical and thrilling endeavor for GE. The firm famous in its FY 2015 Annual Report that “…GE can become a top 10 software company by 2020” and GE Digital is anticipated to “…expand [the company’s] growth rate…[and] improve [the company’s] margins…”

In truth, GE reported in its FY 2016 Annual Report that “Predix-powered and software orders” in FY 2016 have been $four.zero billion. That would put the corporate inside putting distance of cracking the top 10 pure-play software program distributors by income in response to Wikipedia:

{kind=link}

Assuming GE’s FY 2016 numbers for GE Digital are correct, what’s the potential for the enterprise and what worth ought to traders place on this potential by way of the corporate’s share worth?

IIoT Market Forecasts Are…Yuuuuge.

Understanding the potential for GE Digital requires an examination of the enterprise phase’s core market. The market encompassing software program, , and repair options for the seize, transmission, storage, and evaluation of machine-related knowledge is known as the “Internet of Things” (“IoT”). GE, in addition to different massive industrial conglomerates, operates in a subset of the IoT market also known as the “Industrial Internet of Things” (“IIoT”). There are numerous daring predictions concerning the potential dimension and development for the IIoT market. In truth, the varied analysts on the market nearly look like they’re making an attempt to “out-do” one another with increasingly-bolder predictions.

An attention-grabbing article from Forbes contributor Louis Columbus, printed late final yr, captured quite a lot of these predictions, together with some from GE itself. Here are two IIoT predictions summarized within the article and attributed to GE:

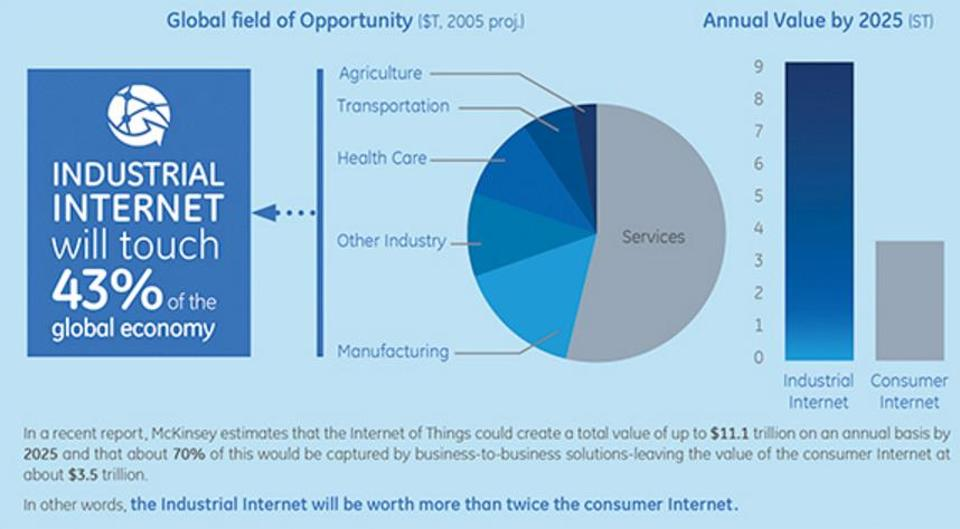

- The Industrial Internet has the potential to ship as much as $11.1T on an annual foundation by 2025. Source: GE Digital, The Emerging Industrial App Economy.

- Investment in infrastructure is anticipated to prime $60 trillion throughout the subsequent 15 years, dramatically rising the general variety of Internet-connected units. Source: GE Announces Predix Cloud – The World’s First Cloud Service Built for Industrial Data and Analytics.

Bolstered by estimates like these, GE went as far as to proclaim a $15 billion gross sales goal for GE Digital by 2020 within the FY 2015 Annual Report:

All of that is definitely encouraging. But do not begin shopping for GE shares simply but…

IIoT Market Forecasts Are… Varied

There are a pair different IIoT predictions from two completely different sources within the Forbes article talked about above which are price examination. (NOTE: the supply knowledge within the first bullet beneath is barely completely different from the information offered within the authentic Forbes article; this knowledge was seemingly up to date after the Forbes article was initially printed):

· The Industrial Internet of Things (IIoT) market was valued at $113.7B in 2014, projected to succeed in $195.5B by 2022 and is anticipated to develop at a CAGR of seven.89% between 2016 and 2022. Source: Industrial IoT Market by Technology, Software, & Geography – Global Forecast to 2022.

· The world industrial web of issues market is projected to succeed in $123.8B by 2021; the market is forecast to develop at a CAGR of 21% by way of 2016 to 2021. Source: Industrial Internet of Things (IIoT) Market Analysis – By Components – Forecast (2016-2021).

These are clearly two very completely different forecasts; and the clever investor ought to subsequently be cautious about placing an excessive amount of religion in them.

Clearly, numerous very good folks assume IIoT goes to be a fully large market alternative. But I can not assist however really feel that the “buzz and hype” element round IIoT might have reached feverish ranges such that the projections for the market will not be reasonable. I recall an e-commerce seminar that I attended in 1998. The speaker proclaimed that any (retail) enterprise that didn’t grow to be an e-commerce enterprise instantly could be “out of business within 5 years.” His basic level on e-commerce as a menace to retail shops was right; however his projection (by way of time) on the broad demise of conventional brick-and-mortar shops was incorrect and excessively bullish on the expansion fee for e-commerce. It appears, to me at the least, that the identical type of extreme bullishness might have contaminated the varied analyst projections for IIoT.

GE Digital Numbers Are… Varied

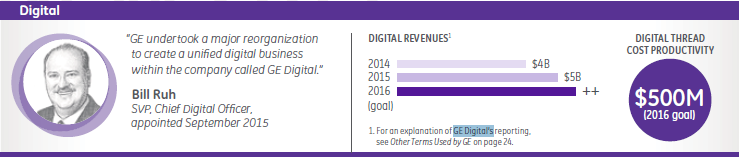

Not solely are IIoT analyst forecasts all around the map, however so are the numbers for GE Digital. In the corporate’s FY 2015 Annual Report, GE stories $5 billion in income for GE Digital for FY 2015:

But within the FY 2016 Annual Report, GE stories $three.6 billion in income for the unit:

![]()

What provides? Did the highest line of the enterprise really decline by $1.four billion? The decline is defined by GE’s modified definition of “what” counts as GE Digital income.

Here is the definition from the FY 2015 Annual Report:

Digital revenues – revenues associated to software-enabled product upgrades, internally developed software program (together with Predix) and related , and software-enabled productiveness options. These revenues are largely generated from our working companies and are included of their phase outcomes.”

And right here is the definition from the FY 2016 Annual Report, with the definition modification italicized:

Digital revenues – revenues associated to internally developed software program (together with Predix) and related , and software program options that enhance our prospects’ asset efficiency. In 2016, we reassessed the span of our digital product choices, which now excludes software-enabled product upgrades. These revenues are largely generated from our working companies and are included of their phase outcomes.”

Personally, I discover this alteration in definition regarding. Is GE Digital only a “bucket” that GE will dump varied income streams into for the looks of development, versus an actual, strategic enterprise unit? In equity, I do assume GE Digital is rather more than only a “bucket,” however the firm’s inconsistent reporting on the efficiency of the enterprise unit is irritating and makes the unit harder to worth.

Don’t Be So Quick To Assume Massive Growth

As I’ve argued in a few my different articles, the software program enterprise as a complete goes by way of important and in lots of instances painful modifications. Generally talking, software program is turning into cheaper by the day and that easy truth is making a drag on income development and driving margin contraction. The underlying causes are quite a few; however definitely the sheer quantity of competitors in any given software program market is a major contributor to the impact seen. GE Digital doesn’t have a monopoly on the IIoT market. Far from it. Virtually each massive expertise vendor is attacking this area, together with IBM (NYSE:IBM), Microsoft (NASDAQ:MSFT), and Amazon Web Services (NASDAQ:AMZN); and there are a lot of smaller gamers all gunning for a “piece of the pie.” (Notably, GE has partnered with Microsoft to supply its Predix platform within the cloud on Microsoft Azure). And this truth would not even think about GE’s industrial rivals, resembling Siemens (OTCPK:SIEGY) and Honeywell (NYSE:HON), who’re additionally ramping up their digital endeavors.

Bulls may level out that despite the fact that GE isn’t the one participant, they’re a number one participant with built-in aggressive benefits, not the least of which is the truth that they really manufacture most of the machines that shall be supported by the GE Digital expertise ecosystem. This is a legitimate argument. GE’s “Digital Twins” software program is exclusive and proprietary to GE, and can assist optimize upkeep and assist of a whole lot of 1000’s of machines manufactured by the corporate by creating computer-generated fashions of the machines that may be analyzed utilizing knowledge generated by the precise machines themselves. This modeling provides GE great alternatives, together with value financial savings from improved effectivity and improved product designs. However, it would not essentially equate to a major driver of top-line development.

Another problem for GE is a slim moat round its Predix platform. Wisely, GE has partnered with varied firms to “fill-in-the-gaps” of its Predix platform, resembling Microsoft for infrastructure (as talked about above) and Splunk (NASDAQ:SPLK) for storage of machine-generated knowledge. While this method makes numerous sense from a go-to-market standpoint, it additionally implies that there are main parts of the Predix system that aren’t proprietary, and that, in flip, will suppress deal margins.

Further, there will not be essentially important and materials variations within the analytical capabilities of the varied expertise firms attacking the IIoT market. The implementation of vendor analytics is usually differentiated by way of velocity or ease of use, however the desired “output” can seemingly be attained with most platforms. So, it is not clear that GE has a tangible, aggressive benefit by way of knowledge evaluation.

Finally, Louis Columbus in one other Forbes article cites that “40% of today’s IoT customers prefer to use traditional and well-established software companies for their IoT solutions.” He goes on to level out that “this represents a challenge for major industrial companies whose future depends on their ability to transition into IoT providers.”

Conclusion

Investors shouldn’t count on unusually excessive development from GE Digital. There are, merely, many headwinds pushing towards the enterprise. Perhaps, for this reason GE didn’t point out its GE Digital forecast of $15 billion by 2020 within the firm’s FY 2016 Annual Report.

I’ve little question that IIoT represents a major market alternative, and GE is rightfully investing to be a pacesetter within the area. But the IIoT market development fee could also be slower than present forecasts predict. Moreover, GE’s inconsistent monetary reporting on GE Digital and lack of clear, sustainable aggressive benefits within the IIoT market ought to make traders extraordinarily cautious when factoring the potential for GE Digital into their valuation of the general firm.

Disclosure: I/we’ve got no positions in any shares talked about, and no plans to provoke any positions inside the subsequent 72 hours.

I wrote this text myself, and it expresses my very own opinions. I’m not receiving compensation for it (aside from from Seeking Alpha). I’ve no enterprise relationship with any firm whose inventory is talked about on this article.

Editor’s Note: This article discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.