Published March 12 by Bob Ciura

The technology industry changes rapidly. Innovation is critically important, to keep up with evolving trends.

For an example of this, consider the cases of Texas Instruments (NASDAQ:TXN) and Intel Corporation (NASDAQ:INTC). On the surface, they seem like very similar companies.

Both Texas Instruments and Intel are large-cap tech stocks, operating in the semiconductor industry. They both manufacture a wide range of chips, that go into a variety of products.

However, their performance has greatly diverged over the past several years.

Those who invested in Texas Instruments stock exactly five years ago, have seen their investment return 148%, not including dividends.

By contrast, Intel’s share price increased just 34% in the same period.

The two stocks have different dividend qualities as well. Texas Instruments is a Dividend Achiever, a group of 271 stocks with 10+ years of consecutive dividend increases.

You can see the full Dividend Achievers List here.

Intel is not a Dividend Achiever.

This article will discuss which of these two semiconductor giants is the better dividend growth stock to buy today.

Business Overview

Winner: Texas Instruments

Both Texas Instruments and Intel have had to undergo major turnarounds in the past several years.

While Intel’s turnaround has been shaky, Texas Instruments’ turnaround has been a huge success.

The reason is because Texas Instruments exited the mobile device market in 2012.

At that time, the company decided it would be more beneficial to focus its wireless operations on embedded markets, which offered greater growth potential.

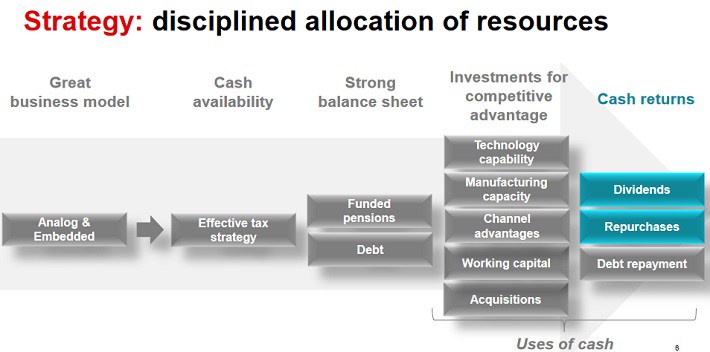

Source: Capital Allocation Presentation, page 6

This proved to be a great decision: Texas Instruments generated $4.1 billion of free cash flow last year. Free cash flow has increased 8% per year on average, since 2004.

Texas Instruments grew earnings-per-share by 24% in 2016.

A critical factor in the decision to exit consumer phones, was the heightened level of competition in mobile chips.

Not only do semiconductor companies compete with each other, but some smartphone device makers like Apple (AAPL) manufacture their own chips.

This is a major difference that separates Texas Instruments and Intel, and explains why their stocks have performed so differently.

Texas Instruments saw the “writing on the wall” with respect to phones and tablets. But Intel pushed ahead in mobile.

It would regret this decision, because staying in mobile cost Intel dearly. Intel lost $3 billion in mobile chip manufacturing in 2013, and lost $4.1 billion in 2014.

Because of the prolonged stagnation of the PC industry, Intel has had to re-focus itself on a new set of growth initiatives.

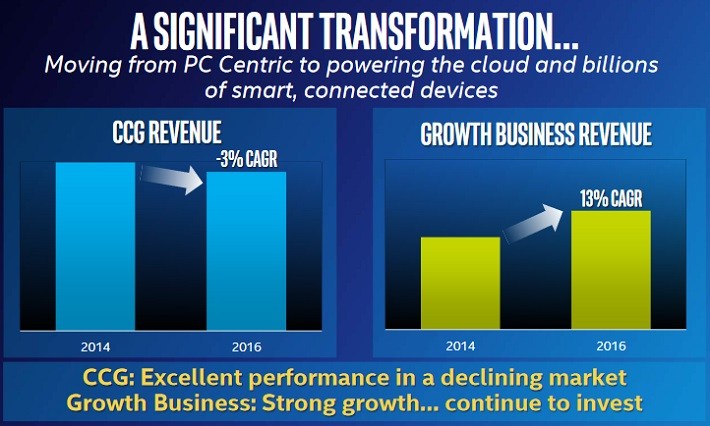

Source: 2017 Investor Meeting Presentation, page 7

Intel’s growth priorities include data centers, and the Internet of Things. These businesses are performing well; Intel’s data center and Internet of Things segments grew revenue by 8% and 15%, respectively.

The problem for Intel is that its core PC business still makes up more than half of its total revenue, which held the company back in 2016. PC revenue increased just 2% last year.

By contrast, data centers and Internet of Things combined, account for one-third of total revenue. Intel needs to increase this going forward, because these are its most attractive growth catalysts.

Growth Prospects

Winner: Texas Instruments

Texas Instruments should have a continued advantage when it comes to future growth potential.

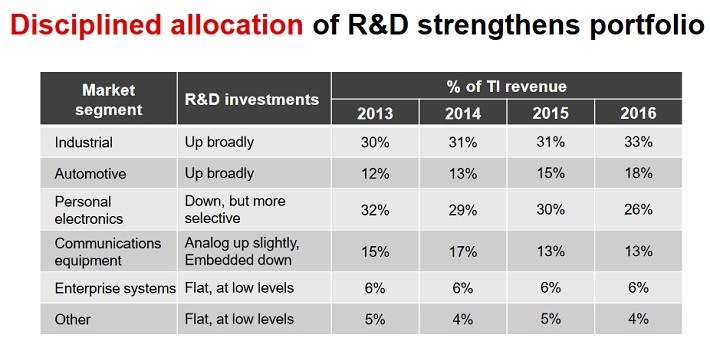

That is because it is increasing investment in two areas where it dominates: Industrial and automotive markets.

Source: Capital Allocation Presentation, page 13

Overall, Intel’s revenue grew 7% in 2016. But higher expenses, including a 5% increase in R&D spending, caused earnings-per-share to decline 9% for the year.

The good news for Intel in 2017 and beyond, is that it still expects low-double digit growth from its major growth segments.

That being said, the company also expects a mid-single digit decline in the PC group. Given the size of this business, this will continue to weigh heavily on Intel.

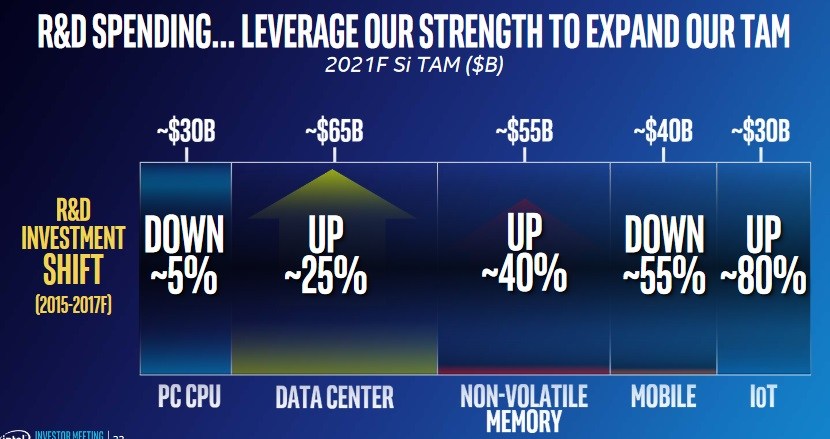

And, the company needs to continue investing more in R&D, to bring the size of its data center and Internet of Things businesses closer to its huge PC segment.

Source: 2017 Investor Meeting Presentation, page 22

Higher R&D spending will weigh on earnings again in 2017.

Not surprisingly, Intel will be reducing research and development spending on PC-related products this year, so that it can devote greater resources to data centers, non-volatile memory, and the Internet of Things.

In addition to cuts in PC-related R&D, Intel will be gutting its investments in mobile—which is also not surprising.

Its huge losses in mobile more than justify this move. If anything, Intel arguably took too long to exit mobile, and its growth has suffered as a result.

Intel expects adjusted earnings-per-share of $2.80 in 2017. This would only be a 2.9% increase from 2016.

Intel’s repeated misfires with its R&D allocation, make Texas Instruments more attractive from a growth standpoint.

Dividends

Winner: Texas Instruments

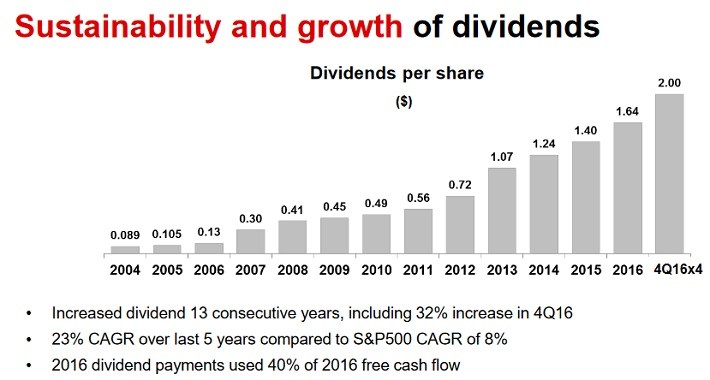

Texas Instruments has increased its dividend for 13 years in a row. And, it has grown the dividend at very high rates.

For example, last year Texas Instruments raised its dividend by 32%.

Intel’s dividend increases have been more sporadic. It has only raised its dividend for two years, after holding its dividend steady for more than two years.

Intel has a slight edge in terms of dividend yield, 2.9% to 2.5%.

But Texas Instruments’ rapid dividend growth rates will easily overcome the difference. In the past five years, Texas Instruments raised its dividend by 23% compounded annually.

Source: Capital Allocation Presentation, page 26

There should be plenty of room for strong dividend growth going forward. Texas Instruments distributed 40% of its free cash flow last year in dividends.

If Texas Instruments continues raising its dividend by 25% per year, investors buying today will generate a 7.6% yield on cost in five years.

This means investors will receive roughly 7.6% of their initial investment in dividend income, five years from now.

Intel’s five-year dividend growth rate is just 4.3%. Assuming 5% annual dividend growth, in five years Intel’s yield on cost will be approximately 3.7%.

In five years, Texas Instruments could provide roughly double the level of dividend income as Intel. As a result, it holds a huge advantage when it comes to dividends.

Final Thoughts

This is a difficult time for Intel. The company is doing the right thing by focusing on higher-growth areas going forward, but it is still weighed down by its huge PC business.

And, it will have to keep plowing more money into R&D, to catch up in areas where it fell behind.

It should not come as a surprise that this is the second matchup in a row that Intel will have lost, to a rival semiconductor company.

Texas Instruments is the better stock for dividend growth investors.

Disclosure: I am not long any of the stocks mentioned in this article.

About the author:

Ben Reynolds

I run Sure Dividend, a website that finds high quality dividend stocks for long term investors using the 8 Rules of Dividend Investing.