(BII)

This story was delivered to BI Intelligence “E-Commerce Briefing” subscribers. To learn more and subscribe, please click here.

Prime members can order on their Echo via a voice search for a restaurant. The Echo will then list the orders that the customer has previously received from that location, and the user can select one of the meals by voice.

Amazon limited the functionality to save users from the drawn-out experience of the Echo having to list all of the menu options by voice for the customer. This demonstrates that voice command isn’t the best interface for every situation — for this use case, visual interfaces like computer screens and touchscreens are still superior to voice.

Amazon Restaurants launched in 2015 and has expanded to 20 different cities in the US. However, online meal delivery services still make up a fraction of the market for takeout restaurant meals in the US today. And even within that small market, Amazon Restaurants trails far behind GrubHub, the clear market leader. In order to gain market share in this small but increasingly crowded sector, Amazon is trying to differentiate itself from competitors with unique features like the Alexa integration that early movers lack.

Pizza chains have long dominated meal delivery, but digital platforms are now enabling the entire restaurant industry to plug into online delivery. In the dominant on-demand meal delivery model, platforms like Grubhub serve as a middleman that connect people to food using the scalability of the internet.

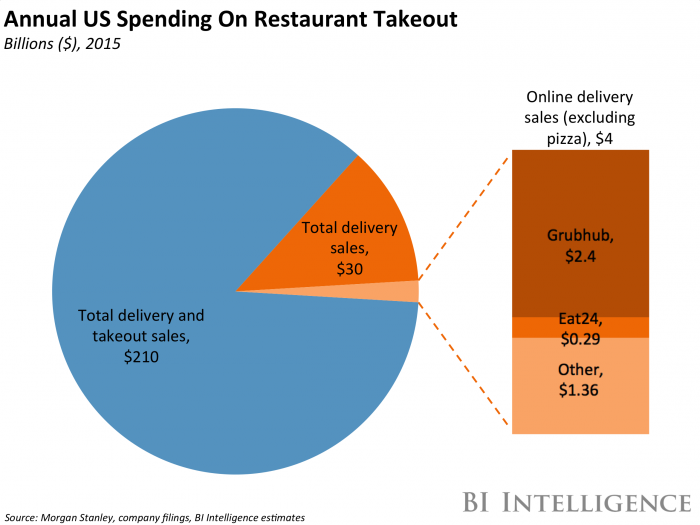

Although some industry leaders are processing hundreds of millions, even billions, in annual food sales volume already, they’re a drop in the bucket in terms of the total addressable market (TAM) for food delivery, which is valued at $210 billion, according to Morgan Stanley Research estimates.

Companies are adopting diverse business models in the market to deliver these meals; some, like Postmates, are focused on the logistics of delivering food, while end-to-end providers like Sprig cook, facilitate ordering, and deliver the food themselves. Ultimately, order-focused platforms like Grubhub/Seamless and Eat24 appear to hold the strongest positions in the market. The former controlled an estimated 59% of total order volume in 2015, while Eat24 held an estimated 7% share. Moreover, Grubhub/Seamless could pose a threat to the logistics companies DoorDash and Postmates if it pushes further into proprietary delivery services, especially in markets its competitors haven’t expanded to yet.

Despite varying advantages and disadvantages, all stakeholders will have to navigate some challenges in the market, including cooling deal volume, consumer resistance to delivery fees, potential industry consolidation, and downward pressure on take rates, which measure the revenue a company actually earns out of the volume they process.

BI Intelligence, Business Insider’s premium research service, has compiled a detailed report for on-demand meal delivery that sizes the market for on-demand meal delivery, outlines the main business models, assesses which key players are in the best and worst position in the market, and also analyzes the underlying risks that all stakeholders will have to navigate.

Here are some of the key takeaways:

- There is a massive unfulfilled market opportunity. As of 2015, about $210 billion worth of food is ordered for delivery or takeout on an annual basis in the US, according to Morgan Stanley Research. But two of the industry leaders, Grubhub/Seamless and Eat24, generated a combined $2.6 billion in food sales last year. This means the market is underpenetrated but massive, which will incentivize continued competition and, potentially, an influx of new entrants.

- There are three main business models that companies adopt. The dominant business model so far has been platform aggregators whose primary function is to support online orders. These include Grubhub/Seamless and Eat24, which control a combined 66% share of the market so far. Other models include delivery-focused logistics models and full-service models in which companies cook the food themselves.

- There are a number of risks that all players in the ecosystem will have to navigate. SpoonRocket, a once promising full-service delivery provider, shut down earlier this year in the face of insufficient capital and intensified competition. This, along with cooling deal volume, could signal upcoming consolidation in the industry. Other risk factors include consumer resistance to delivery fees and lowering take rates, which measure the revenue a company actually earns out of the volume they process.

In full, the report:

- Overviews the on-demand meal delivery market and quantifies the opportunity for expansion.

- Explains the three main business models meal delivery companies adopt.

- Runs through the main competitors in the market and assesses which are in the best position to succeed.

- Identifies the underlying market risks and how they might disproportionately affect certain types of competitors.

To get your copy of this invaluable guide, choose from one of the following options:

- Subscribe to an All-Access pass to BI Intelligence and gain immediate access to this report and over 100 other expertly researched reports. As an added bonus, you’ll also gain access to all future reports and daily newsletters to ensure you stay ahead of the curve and benefit personally and professionally. >> START A MEMBERSHIP

- Purchase & download the full report from our research store. >> BUY THE REPORT

The choice is yours. But however you decide to acquire this report, you’ve given yourself a powerful advantage in your understanding of on-demand meal delivery.

More From Business Insider